Buying or selling a home is an exciting journey, but it culminates in the often intricate and detailed closing process. The closing process is the final step in a real estate transaction, where ownership of the property is officially transferred from the seller to the buyer.

This crucial stage involves numerous steps, including signing various documents, transferring funds, and ensuring all legal and financial conditions are met. In Alabama, the closing process has its unique nuances and legal requirements.

The last stage of the house-buying process is a real estate closing, sometimes referred to as escrow or settlement. It is the formal process through which the seller gives the buyer ownership of the property.

1. Preparing for Closing

When preparing for closing, a buyer or seller needs to work closely with their real estate agents to make sure everything is handled before the deal is closed. Alabama has several specific steps that should legally and contractually be completed.

Offer Acceptance and Contract Signing

Once a buyer or seller accepts an offer, the closing begins. What happens during the initial closing process? A purchase agreement that outlines the terms and conditions of the sale is drafted and signed.

The agreement serves as a legally binding contract between the buyer and seller, specifying details such as the purchase price, closing date, and any contingencies that must be met before the sale can be finalized. Both parties review the contract carefully with their respective agents and attorneys to ensure all terms are clearly understood and agreed upon.

Any necessary negotiations or amendments to the contract are typically addressed at this stage. Once the contract is signed, the buyer and seller can proceed with the next steps in the closing process, confident that the foundation of their agreement is solid and legally sound.

The Role of the Real Estate Agent and Attorney

When selling the house, you can use the For Sale By Owner (FSBO) route or hire a real estate agent and attorney to guide you through the legalities of the process. This also applies to a buyer when you meet a seller who is not going through the MLS to sell their house.

- The real estate agent acts as a liaison between the buyer and seller, coordinating various activities and ensuring that all parties stay informed and on track.

- Agents assist with scheduling inspections, appraisals, and other necessary tasks, providing valuable guidance and support throughout the process.

- Attorneys provide legal expertise, reviewing contracts and documents to ensure compliance with Alabama state laws. They also address any legal issues that may arise, such as title defects or disputes over contract terms.

Gathering Necessary Documents

Documents form the foundation for home sales as much as any other transaction. Working with a real estate agent or attorney ensures that these documents are compiled and reviewed early.

- Buyers will need to provide financial information, including proof of funds and loan pre-approval letters.

- Sellers must supply documentation related to the property, such as the title deed and any existing mortgage statements.

Other documents may include home inspection reports, appraisal results, and any disclosures required by law.

2. Title Search and Title Insurance

A property title has all the history of the property and can show any liens, encumbrances, or other claims that could affect the transfer of ownership. A title search is conducted to verify the legal ownership of the property as well.

A title insurance serves as a safeguard against any future disputes or claims related to the property’s title. It protects buyers and lenders from potential financial losses arising from title defects that were not discovered during the initial search.

How Do They Work?

In Alabama, the title search is typically performed by a title company or a real estate attorney. The results of the search are compiled into a title report, which is reviewed by both the buyer and seller.

While the title search aims to identify any issues, there is always a possibility that some problems may go undetected. Title insurance provides a safety net, covering the costs associated with defending against claims or rectifying title defects that may arise after the purchase.

In Alabama, buyers typically purchase an owner’s title insurance policy, while lenders require a lender’s policy as a condition of financing. These policies offer protection against various risks, including errors in public records, undisclosed heirs, and fraudulent claims.

3. Home Inspection and Appraisal

A home inspection serves as an assurance of the soundess of the property for both the seller and buyer. An appraisal also provides essential information on the condition and value of the property.

They are both done by licensed professionals in Alabama to give a common flat foundation to complete the sale.

Why Is a Home Inspection Done?

A home inspection is a thorough examination of the property’s physical condition, conducted by a qualified home inspector. This evaluation covers various aspects of the property, including the structure, electrical systems, plumbing, roofing, and more.

- Buyers get critical insights into the property’s condition, highlighting areas that may require repairs or maintenance. It offers an opportunity to negotiate with the seller for necessary fixes or adjustments to the purchase price.

- Sellers can benefit from a pre-listing inspection by addressing issues upfront, potentially making the property more attractive to buyers and reducing the likelihood of surprises during the closing process.

The goal is to identify any existing or potential issues that could affect the property’s safety, functionality, or value.

Why is An Appraisal Done?

An appraisal is an unbiased assessment of the property’s market value conducted by a licensed appraiser. Unlike a home inspection, which focuses on the property’s condition, an appraisal considers various factors such as location, size, condition, and comparable sales in the area to determine the property’s fair market value.

The valuation is handy for both buyers and lenders as it ensures that the property’s price is in line with its worth. You wouldn’t want to buy a house that is listed for double the market price, especially if the house hasn’t been appreciated.

If the appraisal value is lower than the agreed purchase price, it may necessitate renegotiations with the seller or adjustments to the financing arrangements.

4. Financing and Mortgage Approval

Securing financing involves obtaining a mortgage to fund the purchase, which requires a thorough review of the buyer’s financial situation by the lender. Mortgage approval ensures that buyers have the necessary funds to complete the transaction, making it a cornerstone of the closing process.

In Alabama, the financing process is governed by state-specific regulations and lender requirements.

Steps to Secure Financing

The first step in securing financing is obtaining a mortgage pre-approval from a lender. Pre-approval involves an initial assessment of the buyer’s financial situation, including income, credit score, and debt-to-income ratio.

Pre-approval provides an estimate of the loan amount the buyer can qualify for, helping them set a realistic budget for their home search. Once the buyer finds a property and has an accepted offer, the formal mortgage application process begins.

This involves submitting detailed financial documents, such as tax returns, bank statements, and employment verification, to the lender. The lender will then conduct a thorough review, known as underwriting, to assess the buyer’s ability to repay the loan.

Pre-Approval vs. Final Mortgage Approval

Pre-approval and final mortgage approval are two distinct stages in the financing process.

- Pre-approval is an initial determination of the buyer’s creditworthiness and borrowing capacity, based on preliminary information provided by the buyer. It gives buyers a clear idea of their budget and strengthens their position when making an offer on a property.

- Final mortgage approval occurs after the lender has conducted a comprehensive review of the buyer’s financial documents and the property itself. This stage includes verifying the buyer’s income, employment, and credit history, as well as appraising the property to ensure it meets the lender’s criteria.

Once all conditions are met, the lender issues a commitment letter confirming the loan’s approval and outlining the terms and conditions of the mortgage.

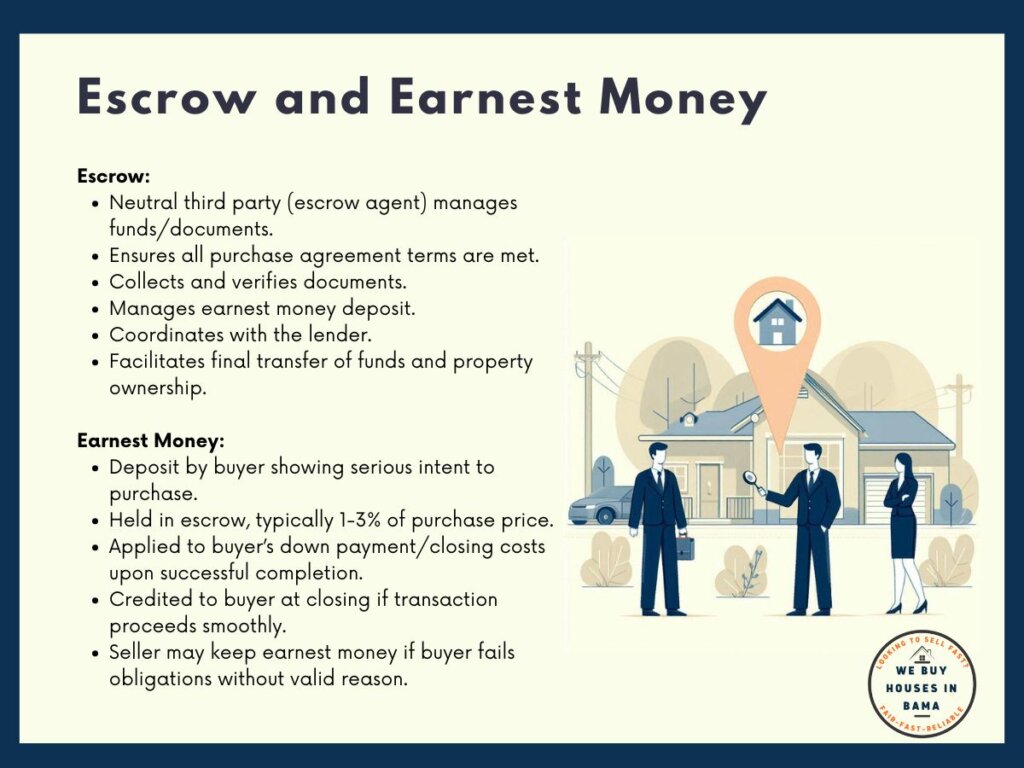

5. Escrow and Earnest Money

Escrow and earnest money provide security and assurance to both buyers and sellers. Escrow refers to a neutral third party holding funds and documents until all conditions of the sale are met, ensuring a fair and orderly transaction.

Earnest money, is a deposit made by the buyer to demonstrate their commitment to purchasing the property.

How Does Escrow Work?

Escrow is a legal arrangement in which a neutral third party, known as the escrow agent, holds and manages funds and documents on behalf of the buyer and seller until all the terms of the purchase agreement are fulfilled. The escrow agent ensures that all conditions of the sale are met before disbursing funds and transferring ownership of the property.

The escrow agent handles various tasks, including collecting and verifying documents, managing the earnest money deposit, coordinating with the lender, and facilitating the final transfer of funds and property ownership.

How Does Earnest Money Work?

Earnest money is a deposit made by the buyer to demonstrate their serious intent to purchase the property. This deposit, typically a percentage of the purchase price, is held in escrow and applied toward the buyer’s down payment or closing costs upon successful completion of the transaction.

The amount of earnest money required can vary, but it generally ranges from 1% to 3% of the purchase price. If the transaction proceeds smoothly, the earnest money is credited to the buyer at closing.

However, if the buyer fails to fulfill their contractual obligations without a valid reason, the seller may be entitled to keep the earnest money as compensation for the lost opportunity and time.

6. Closing Day Procedures

The last stage of the house-buying process is a real estate closing, sometimes referred to as escrow or settlement. It is the formal process through which the seller gives the buyer ownership of the property.

What to Expect

The process typically takes place at the office of the closing agent or attorney, although remote or electronic closings are becoming more common. Buyers and sellers will review and sign numerous documents, including the deed, loan documents, and settlement statement.

The closing agent will guide both parties through the paperwork, answering any questions and verifying that all documents are properly executed.

- The deed transfers ownership of the property from the seller to the buyer. The deed must be signed by the seller and notarized to be legally binding.

- The mortgage note and deed of trust is signed by the buyer if financing is involved.

- The settlement statement, also known as the Closing Disclosure, outlines all the financial details of the transaction, including the purchase price, closing costs, and the distribution of funds.

- Additional documents may include affidavits, disclosures, and any specific forms required by Alabama law or the lender.

Transfer of Funds and Ownership

The buyer will provide the necessary funds for the purchase, which may include their down payment, closing costs, and any remaining balance on the purchase price. These funds are typically wired to the closing agent’s escrow account, where they are held until all conditions of the sale are met.

Once all documents are signed and funds are verified, the closing agent will distribute the funds to the appropriate parties. This includes paying off the seller’s existing mortgage, disbursing real estate agent commissions, and covering any closing costs.

The deed is then recorded with the local county office, officially transferring ownership to the buyer. The buyer will receive the keys to the property, marking the successful completion of the transaction.

The Role of Home Inspections in the Buying Process

A real estate closing in Alabama involves various processes and documents that are require completion to avoid any legal hiccups. This can be avoided by working with experienced real estate agents and attorneys.

This article is not meant to provide legal advice but to give an overview of Alabama’s closing process as the laws vary in different states. Another important part of real estate transactions are the home inspections done to verify the conditions of the homes.

As mentioned lightly earlier, a deeper understanding of home inspections can significantly affect the deal you get as a buyer for your house. As a buyer, home inspections reveal hidden damages or areas of concern that can be addressed before the deal is closed.